Price increases has been the news around the industry lately, ending 2020 and starting off 2021. Cooper Lighting was the first big player that we reported on to announce their price increase, and they were followed by: Maxlite, TCP, Signify, Acuity, QSSI, and Hubbell.

In order to provide some more insight towards these trends, William Blair and Channel Marketing Group surveyed electrical distributors, manufacturers, and lighting agents in December 2020 about the state of their operations and their outlook for the future. Among these topics were that of pricing trends and quotation activity, which will be the focus of this article. The survey audience was put into three different categories: Distributors, Manufacturers, and Reps/Agents.

Pricing Trends

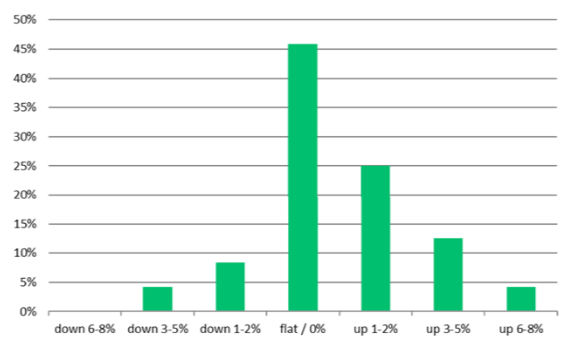

Distributors:

Distributors largely reported a flat market, but behind that there were more reporting an increasing trend rather than decreasing. The reported weighted average shows an increase of .9%.

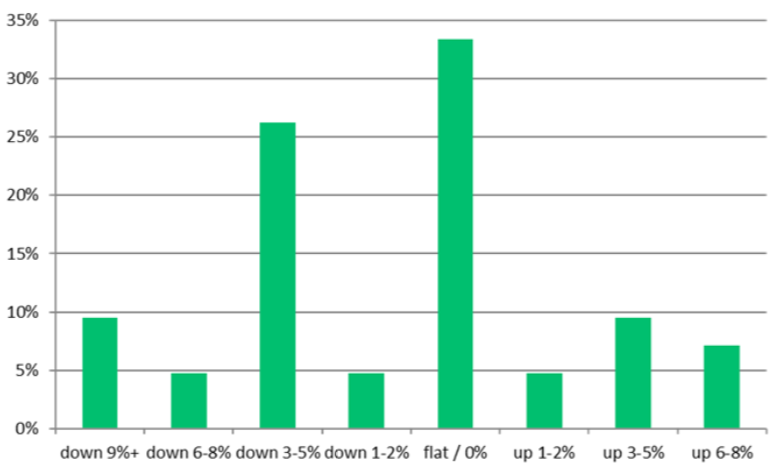

Manufacturers:

Manufacturers also largely reported a flat market, but this was followed by more reports of a decrease rather than increase. The weighted average shows a decrease of -1.74%, the largest decrease of the three groups.

Reps/Agents:

Like Manufacturers, Reps/Agents also reported a flat market followed by a decreasing trend. The weighted average shows a decrease of -1.45%.

Despite the recent headlines of major players all implementing price increases, it seems they are not an indicator of what direction the entire industry will take, as more survey participants saw flat or decreasing price trends rather than an increase.

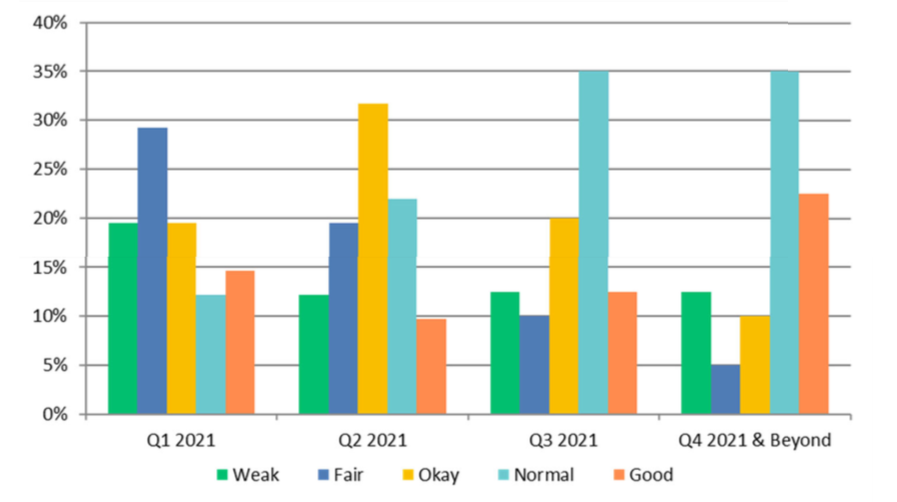

Quotation Activity

William Blair and Channel Marketing Group made a clarification that the data collected is “lighting quotation activity based upon project ship date, looking into 2021. It is unknown if these projects are funded or unfunded and is solely quotations, not confirmed sale.”

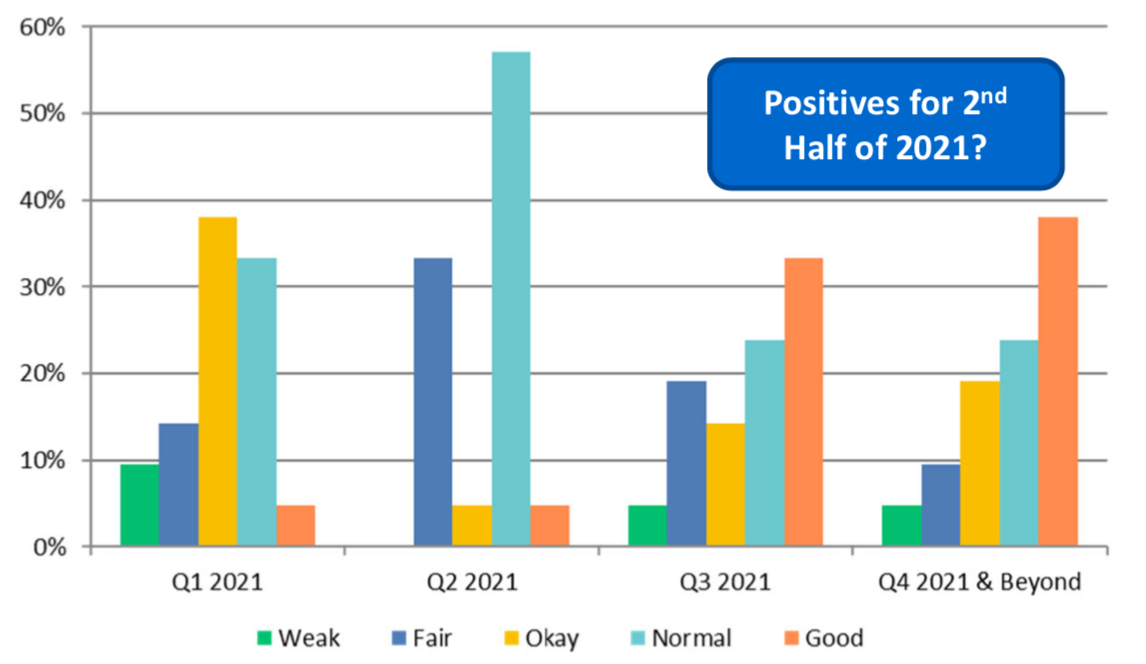

Distributors:

Distributors forecast largely normal quotation activity for lighting jobs for Q1 and Q2 2021, but showed a lot more confidence for the second half of 2021. The reported weighted average is 3.3%.

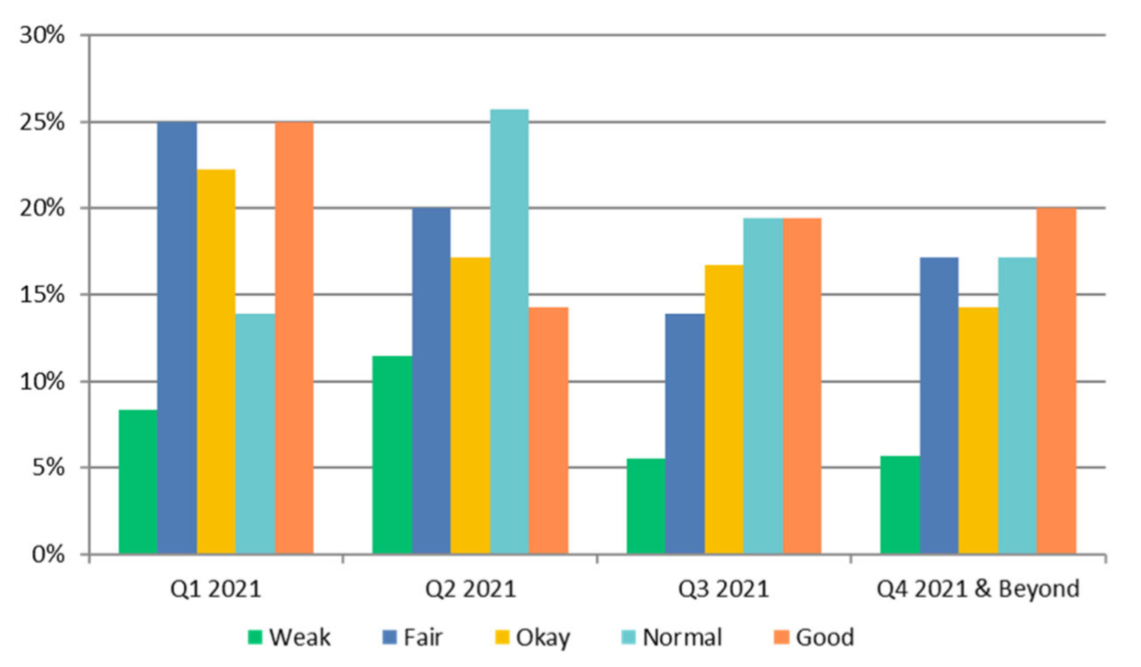

Manufacturers:

Manufacturers reported higher confidence for the first half of 2021 than Distributors, however the opposite is true for the later half of 2021. Willam Blair and Channel Marketing Group explained the lower confidence of manufacturers saying “This could relate to visibility of projects that could happen (especially for the renovation market) as well as knowledge about projects that have been delayed and could resurface.”

Reps/Agents:

Reps/Agents saw a weaker forecast than either of the two groups. The first half of the year saw Fair and Weak forecasts, with the later half mainly forecasting just a return to normal. Although, greater confidence was reported for Q4 2021 and beyond.

Reps/Agents saw a weaker forecast than either of the two groups. The first half of the year saw Fair and Weak forecasts, with the later half mainly forecasting just a return to normal. Although, greater confidence was reported for Q4 2021 and beyond.

Overall, it seems the industry has an optimistic outlook for quotation activity and business volume, but many do not see an increase in pricing alongside it. These results are interesting, given numerous recent headlines regarding price increases. It will be interesting to see how the year plays out and what the state of industry will actually be throughout 2021 as the world hopefully recovers from the pandemic. We would like to thank William Blair and Channel Marketing Group for sharing their findings with us and allowing us to report on them.